.png)

Building a successful cloud and growing it quarter after quarter, year after year, with first mover status or without it, is not an easy task. It helps to have other businesses to fund a cloud, which is why Amazon Web Services and Google Cloud are as big as they are in cloud today.

But perhaps in the longest of runs, having millions of platform and application customers will matter more, particularly as companies want to add AI functionality to their applications or rework their businesses from the ground up to use AI. And this is why Microsoft has been able to grow its hybrid cloud platform, which spans on premises Windows Server and on cloud Azure, faster than many expected. Microsoft might not have had first mover status in AI, but it has clearly been able to invest enormous sums in infrastructure and partnerships like the one that it has with OpenAI, and its financials reflect this.

Being The Next Platform, we look at the clouds as well as the suppliers of semiconductors or systems through the lens of how much money they get from datacenter platforms, and we are always particularly interested in the base systems that companies sell – meaning servers, switches, storage, operating systems, core middleware, and financing – either on premises, in the cloud, or in a hybrid fashion. It is tricky trying to figure out the revenue and profits for the “real” or “core” datacenter systems at the OEMs and clouds of the world, but we give it our best shot every quarter so we can get a better sense of what is happening in the datacenters of the world.

And as far as we can tell, Microsoft has the largest platform business in the world, and it is also the most profitable of the three big clouds based in the United States.

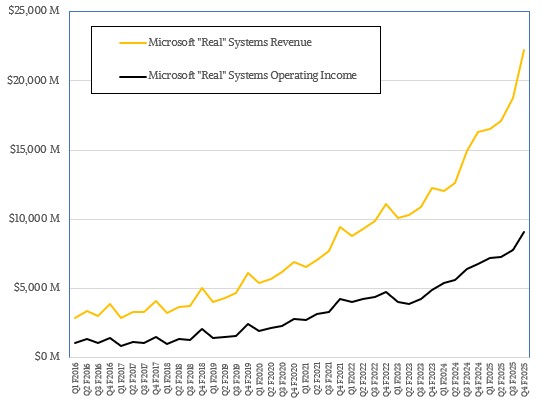

In the quarter ended in June, which is the end of Microsoft’s fiscal 2025 year, the company had total sales of $76.44 billion, up an amazing 18.1 percent, with operating income of $34.32, up 22.9 percent and representing 44.9 percent of revenues. A lot of this revenue at Microsoft happens above the operating system level and on PCs, and thus does not count as “real” systems. If you do a lot of spreadsheet magic to extract all of that out, we think the core Microsoft systems business, including Windows Server and Azure platforms, brought in $22.27 billion, up 36.8 percent, and had operating income of $9.05 billion, up 34.5 percent and representing a very solid 41.5 percent of systems revenues.

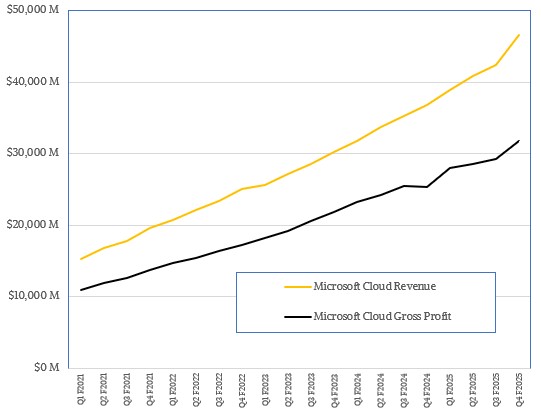

Microsoft’s overall cloud revenues are much larger than this, since it sells a lot of PC and server applications as cloud services above and beyond the PC and server systems software it also sells. In the quarter, Microsoft’s overall cloud sales came to $47.69 billion, up 27 percent, and gross profits (which it reports and which we wish were operating income instead) were $31.75 billion, up 25.2 percent.

And just to be clear, Microsoft Cloud does not mean Microsoft Azure, which is what we used to call a public cloud where you can rent infrastructure. Based on our model, we think Microsoft’s Azure cloud services drove $19.34 billion in sales (up 39 percent), with operating income of $8.25 billion, up 43.4 percent and representing 42.7 percent of sales.

Everybody is enthusiastic about AI in terms of how Microsoft has invested heavily in it, how Azure has been boosted by it, and how the Dynamics and other applications that are being outfitted Copilots with AI functionality, but we really don’t have a sense of how much money the company is spending on AI and how much it is deriving from AI. Six months ago, Microsoft said its total AI business had an annual run rate of $13 billion, somewhere just shy of 20 percent of revenues, and it could be higher now.

Trying to calculate the size of the “real” base systems business within Amazon Web Services is a little trickier, mostly because AWS does not talk about itself in a way that easily lets us abstract higher level application software from underlying infrastructure hardware and software. (And as with Microsoft, it is hard to decide what parts of the AI stack are infrastructure and what parts are really applications.)

In the second quarter ended in June, the big Amazon company that sells stuff, makes media, promotes stuff, and rents out IT infrastructure brought in $167.7 billion in sales, up 13.3 percent, and $136.8 billion of that was not from the AWS compute and storage utility.

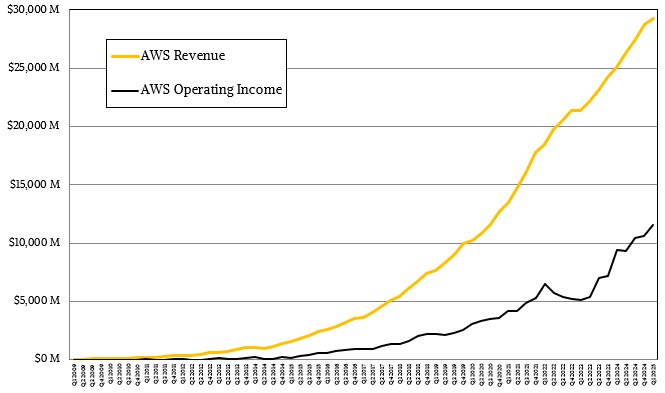

The AWS unit had $30.87 billion in revenues in Q2, up 17.5 percent year on year, and had an operating income of $10.16 billion, up 8.8 percent. AWS represented 18.4 percent of Amazon’s revenues, but 53 percent of its operating income, which is another way of saying that by paying the premium for AWS cloud infrastructure, you are paying so Amazon the retailer and media mogul can get its IT capacity for a whole lot less money than you. (One might even say it is “free” give that the profits are probably larger than the IT budget for Amazon, the parent.)

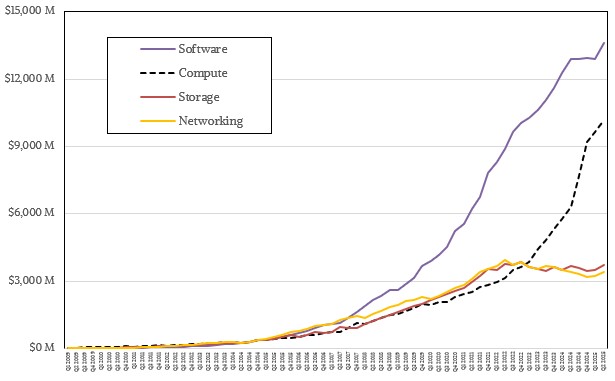

We can only insinuate the “real” AWS systems business by making estimates of how much compute, storage, networking, and software AWS sells each quarter, and here is what our plot looks like:

Before the GenAI boom started in late 2022, compute was on the wane and software was ascendant. We think – and it is as much a hunch as anything else – that as GPU and XPU compute has been on the rise thanks to the first phase of AI and now GenAI, revenues from networking and storage flattened out. If you have a better model, please share and explain. We do think that eventually AWS will have to give some color on this.

In Q2, we think the “real” datacenter systems revenues for AWS were on the order of $17.3 billion, up 29 percent, and operating income was around $4.8 billion, up 19.5 percent. This is smaller than the Microsoft systems business, as we have been pointing out for some time.

We do know that AWS is spending humungous sums on capital equipment, and we think that most of this is for datacenters and their gear and not for Amazon warehouses for the retail business.

In the quarter, AWS spent $33.1 billion on capital expenditures, and we think somewhere around $28 billion of that was for IT infrastructure. And within that, maybe $25.9 billion of that was for AI infrastructure.

No one outside of AWS knows how much revenues AI drives for the cloud provider, and saying that it is multiple billions of dollars and growing fast, as the company has said, doesn’t really tell us much. We think that is a low-ball figure. If AWS is on track to spend maybe $100 billion on IT gear and most of that is for AI processing, we presume it is making many tens of billions of dollars in revenues from AI hardware rental, and then billions of dollars for software and services on top of that.

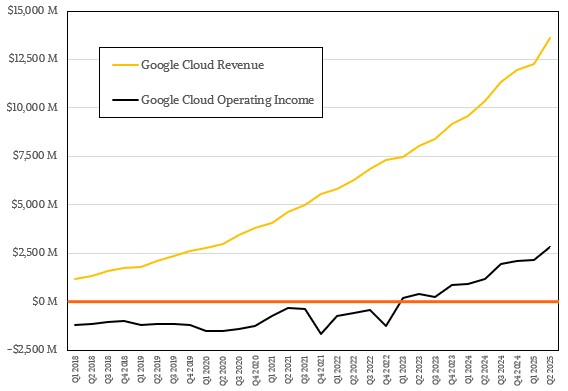

That leaves us with Google, which brought in $96.43 billion in revenues in Q2, up 13.9 percent, and had an operating income of $31.27 billion, up 14 percent, and net income of $28.2 billion, up 19.4 percent.

Google Cloud brought in $13.62 billion of revenues, a mere 14.1 percent of Google’s revenues, and posted $2.83 billion in operating income, up by a factor of 2.4X year on year. This was 9 percent of the operating income of the whole of Google. (We don’t call it Alphabet.) Google remains a search and advertising business with a growing cloud business that represents all of its “real” systems business.

But, as we have also pointed out many times, Google could sell all of its gear to Google Cloud, make itself the primary customer of Google Cloud, and suddenly the Google Cloud would be a whole lot bigger and as profitable as Google wanted to show it to be.

Sign up to our Newsletter

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now