.png)

Recently, we discussed how some technology isn’t really useful as a technology, but rather is useful because it greases the wheels of politics.

Imagine a society where any time you wanted to change the law, you had to invent some new technology in order to change it. Like, let’s say the society has a law on the books that says people who wear green shorts are not allowed to go swimming in a public pool, and everyone more or less agrees that this is kind of annoying but the law can’t be changed. And then someone creates something that works exactly like a swimming pool but they call it something else, let’s say a beeblebrox. Now people who wear green shorts can go swimming in the beeblebrox, and the law about swimming pools is still on the books. And, you know, if anyone ever points out that a beeblebrox is the same thing as a swimming pool, the guys who use the beeblebrox will point out that in fact it is a very different thing. After all, just look at the name! Beeblebrox sounds nothing like swimming pool.

…

More specifically:

We have a society where, for a lot of reasons, there is a lot of regulation on how people can transact;

Much of that regulation may do more harm than good, but our legislative system moves slowly and favors doing nothing over doing something;

Crypto is just complicated enough that everyone’s eyes glaze over when people describe it, and so you can sneak it in by pretending it’s not doing the thing that everyone uses it for and therefore avoid regulation.

I think that last point is really critical. You don’t need the complicated blockchain to solve these tasks…But actually you really do still need the complicated blockchain tech, the complicated blockchain tech is the most important part, because that is the only way to convince everyone that this is beeblebrox and therefore the previous rules don’t apply.

Tech Things: the point of crypto is breaking the rules

Imagine a society where any time you wanted to change the law, you had to invent some new technology in order to change it. Like, let's say the society has a law on the books that says people who wear green shorts are not allowed to go swimming in a public pool, and everyone more or less agrees that this is kind of annoying but the law can't be changed.…

In many cases, these companies and industries are exploiting a pretty simple risk arbitrage. Let’s say you wanted to start a company that offered taxi-like services. Just for convenience, let’s give the company a name, say “Uber” (I just randomly came up with that name, any relation to real companies is coincidence). Starting Uber as a taxi service would expensive because you’d need to meet all sorts of regulatory requirements. So a lot of people don’t do it. But if you have an appetite for risk, you can start your taxi company without meeting any of those regulatory requirements and just…hope it goes ok? The risk is that the government will crack down on your business and possibly send you to jail. But the reward is that you can beat literally everyone else in the industry because they are all trying to follow regulations and you’ve decided a priori that Uber is not going to do that. It’s a bit like that old saying that “a parking ticket isn’t a penalty, it’s just the price of parking there.” Most of the time, that price is too high. But sometimes it makes sense to gamble on getting the ticket.

It turns out there is an entire class of extremely valuable tech companies that are basically just exploiting risk arbitrage. Uber, obviously. AirBnB. Doordash, possibly. The entire crypto industry. In each of these cases, the underlying company is using technology as a fig leaf, a way to give plausible deniability when regulators come knocking. And in each of these cases, the fig leaf worked! Or at least, it worked long enough that the companies were able to grow to a size where prosecuting them would be awkward and difficult.

What if…you didn’t even bother with the fig leaf? What if you don’t care at all about regulatory scrutiny?

The basic structure of such an enterprise might look something like this:

Pick an extremely regulated industry

Build a company that does exactly what companies in that regulated industry do, no fancy technology required

Call it something else

Profit

This is basically how I feel about Klarna. Klarna IPO’d about a month ago, which I somehow completely missed. On opening day, it was valued at $20 billion. It dropped a bit since then, it’s currently $15b.

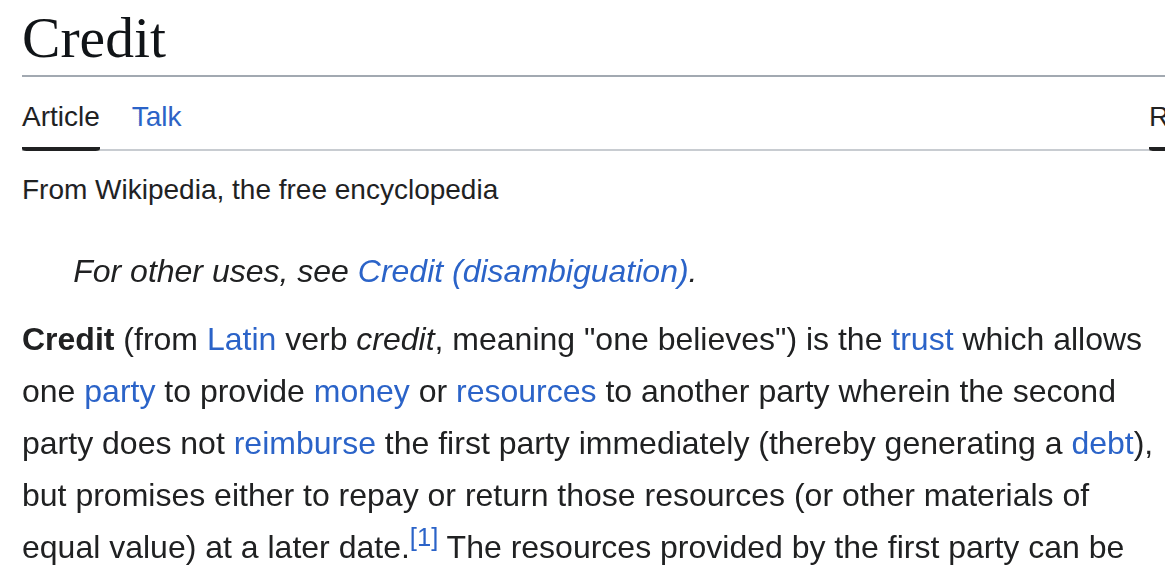

What does Klarna do? Klarna does credit. If you ask Klarna what they do, they will insist that they do something completely different, called “Buy Now, Pay Later.” If you ask what “Buy Now, Pay Later” is, Klarna will say that it is a novel financial technique that allows someone to buy a thing now, and then pay it later. If you ask how this is different from credit, Klarna will presumably get mad at you and tell you to take a hike. And if you ask a five year old what credit is, they may think for a minute and then come back and say “it’s when you buy something now and then pay it back later.”

Now, there can be good reasons to skirt regulation (not an endorsement!). But it’s risky. Sometimes, that regulation is there to protect your consumers and constrain your ability to do things because they have vast unexpected societal harms. And other times, that regulation is there to help the company, by clearly demarcating rakes that other companies have stepped on before to devastating effect. For example, the credit industry has a ton of regulations related to credit scores. Those regulations exist to protect consumer banks from bad debt. If a bank loans me credit, and I do not pay it back, that will impact my credit score which makes it harder for me to get more credit later. If the bank didn’t use credit scores and instead loaned everyone bad debt, and no one could pay it back, that would impact the world economy and everyone would be very sad. So there’s a lot of incentive to use credit scores to make sure people do not get bad debt.

Right, well…

From PaymentsJournal:

For now, Klarna and Afterpay have declined to participate in the new credit scoring model that incorporates consumers’ buy now, pay later (BNPL) loan information…

The companies said credit bureaus aren’t receiving real-time, accurate data on BNPL loans, which could negatively impact consumers’ creditworthiness.

“A strong differentiator for BNPL products is to be a way for their customers to use a form of credit without having to necessarily rely on the stricter underwriting of a credit card,” said Ben Danner, Senior Credit and Commercial Analyst at Javelin Strategy & Research. “This is built into the fabric of BNPL firms’ marketing strategies.”

“I see two main issues,” he said. “First, Klarna and Afterpay view the current scoring models as built on the legacy of credit cards and these models are not updated to reflect the novelty of BNPL. Second, Klarna and Afterpay want FICO to guarantee that the scoring data will not penalize the scores of their customers.”

Klarna does not use credit scores, because they claim they are not a credit institution. They are “Buy now, pay later.” This may lead to some problems.

Let’s say I was feeling hungry one day, and I wanted to buy a Doritos Locos Taco from Taco Bell. And let’s say I go and use Klarna, which will split my $2.69 order into 4 payments of ~68 cents. What if I just…miss a payment? Is my taco just free? On the one hand, no. Klarna requires you to have a card filed with them and they will charge your card an exorbitant interest rate if you miss a payment. But on the other hand…if you cancel your card, or if you put in a temporary card from one of those temporary card services that auto-expires, what is Klarna going to do? They can’t, like, claw back the taco. By the time Klarna realizes that you can’t / won’t pay, that taco is 30 days digested. (Not an endorsement!)

This is the same problem all credit companies have. Normally, credit-giving institutions get around this obvious problem by capping your initial credit, only increasing your credit line after a history of purchases and payments, and demanding a lot of personally identifying information to make sure that your credit score is tied to you forever.

As far as I can tell, Klarna doesn’t do any of this? [EDIT: but Sam in the comments disagrees, see below for the link to the F1, which discusses their methods for underwriting risk] You can just, like, keep making Klarna accounts and buying tacos and never paying them off. Which, of course, is bad for Klarna. From NBC:

Klarna’s customers are having a harder time paying back the installment loans they take out with the popular “buy now, pay later” service.

The Swedish company’s net losses doubled in the first quarter even as its user base and revenue grew Klarna reported Monday, weeks after pausing its plans to go public over concerns about tariffs and economic uncertainty. Klarna’s consumer credit losses swelled 17% in the first quarter from the same period a year earlier, hitting $136 million.

Industrywide, BNPL borrowers are increasingly falling behind on their loan payments. In a survey conducted by the credit platform LendingTree last month, 41% of users said they paid late within the last year, up from 34% the previous year.

In some sense, this is totally obvious. Klarna is specifically targeting people who cannot get past the stricter underwriting requirements of the normal credit system, which, besides being predatory, seems…obviously bad for Klarna? The only people who are going to be financing a Doritos Locos Taco are the people who couldn’t get good credit lines to begin with! Klarna is self-selecting into giving loans to exactly the people who cannot pay back those loans. And as more people realize that they can abuse Klarna for free stuff — because, again, there does not seem to be a downside — more people will sign up, juicing Klarna’s growth numbers and further hurting its bottom line.

All of this reminds me of MoviePass. For those who forgot, MoviePass was the greatest startup ever created. The premise was that you would get to watch unlimited movies in theaters for $20 per month. MoviePass didn’t have any deals with the theaters or anything like that. It was just paying the theaters full price. In NYC, the price of a single movie ticket is about $20. So if you saw a single movie in NYC using MoviePass, the company would break even, and any movie after that would be free for you and pure loss for MoviePass. For a brief 3 month period, MoviePass shoveled VC money directly into the NYC cinephile community, and it was glorious.

MoviePass eventually shut down because you can’t sell a dollar for 75c and expect to stay in business for very long. I think the same is true of Klarna. Frankly it’s a miracle that they made it to IPO. Now that they are here, I expect they will clamp down on their loose reporting rules and start treating things more like an actual credit card company.

Not that that will stop the free taco train.

These days, there’s an entire industry of ‘buy now, pay later’ companies. In theory, you could keep making free accounts and keep getting free tacos for a long time. Not an endorsement!