.png)

Every fund must eventually close. But with SEBI’s 2024 stricter rules and timelines, how transparently it’s managed now defines a manager’s credibility. This blog explains how to handle closures smartly and build trust for the next fund by meeting LP expectations.

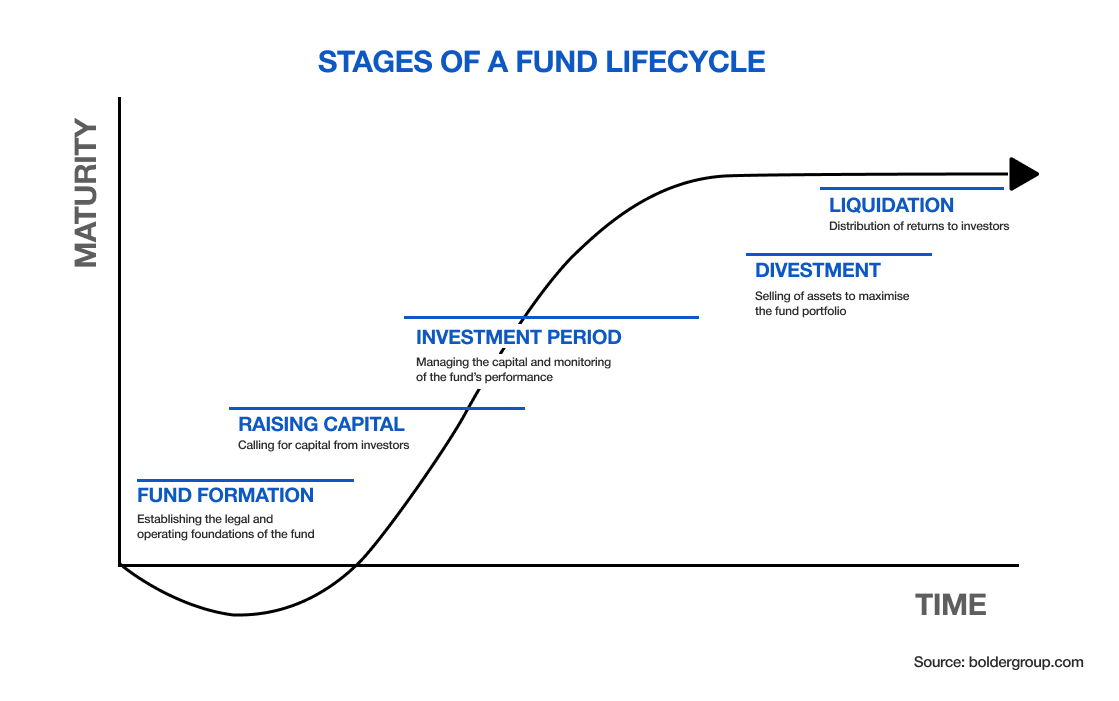

Most conversations in private equity and venture capital focus on raising capital, making investments and chasing successful exits. However, every fund eventually reaches another milestone - closure.

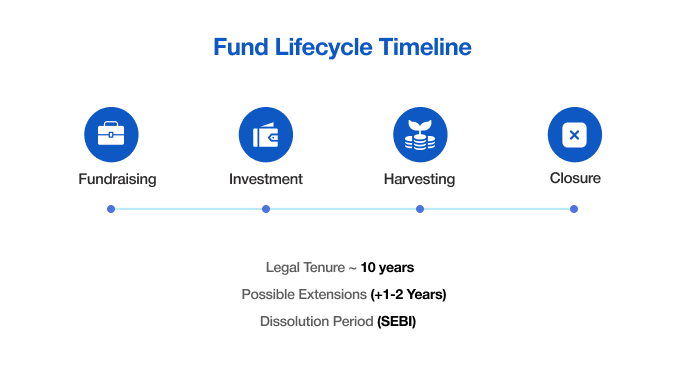

The ticking clock of fund lifecycles

From the moment a fund is launched, the clock starts ticking. Most funds are designed to last around 10 years, with short extensions in certain cases. As the end of the term nears, investors expect their capital to be returned. How a manager handles this final stage plays a pivotal role in shaping their reputation, just as much as their fundraising or investment track record.

While extensions are possible, they are no longer indefinite. SEBI tightened regulations in 2024, emphasizing the importance of timely distribution or closure. By the end of the liquidation period, managers must either return capital, secure 75% investor approval to enter a “dissolution period,” or distribute any unsold assets in-specie.

“Zombie funds are no longer an option under SEBI’s 2024 rules.”Why the end matters

Fund closure, being a legal formality, is a pivotal opportunity to showcase efficiency, transparency and execution. LPs expect transparency and adherence to fiduciary duties, including ensuring that carry, claw backs and disclosures are honored until the very last day. They also value efficiency when a closure maximizes what can be returned while winding down in an orderly way. But closure is about managing it strategically rather than getting through it. How the remaining assets are handled can leave a lasting impression on investors.

What happens when assets remain

It’s rare for a fund to close with every portfolio company neatly exited. In most cases, some assets will still be maturing or facing liquidity challenges. Managers typically have two main options:

- Sell Remaining Assets: This approach is straightforward and provides liquidity for distribution to investors. However, it may mean missing out on potential upside if the assets are sold prematurely.

- GP-Led Continuation Vehicles: In this option, the GP rolls certain assets into a new fund. LPs can then choose to either cash out immediately or continue their investment. While this strategy is becoming more common, it requires fairness opinions and oversight by the LP Advisory Committee (LPAC) to maintain trust.

In some cases, liquidity challenges are linked to specific investors, which is where LP-Led Secondaries can come into play. These transactions allow investors to sell their stakes without affecting the underlying assets.

When all else fails, managers may resort to in-specie distributions, handing over company shares directly to LPs. This option preserves future upside but is often unpopular as many LPs prefer liquidity over holding private company shares.

The compliance backdrop

In April 2024, SEBI introduced the “dissolution period” as a formal tool. It requires investor approval, transparency, and prohibits management fees during this period. Funds whose liquidation period had expired on or before July 24, 2024, were permitted to seek extensions running up to April 24, 2025. If assets remain unsold after the dissolution period, they must be distributed in-specie.

Regulators are increasingly focusing on fund closures. Valuation practices and disclosures are under scrutiny, sending a clear message that compliance continues until every rupee is returned.

The global rise of continuation funds

Secondary markets have become an essential part of fund closure strategies. In 2024, global secondary transactions reached a record USD $156–162B, with GP-led deals accounting for around $70–75B. By the first half of 2025, GP-led deal volume surged by 60% year-on-year, totaling approximately $46B.

The APAC region, including India, has become one of the most active markets for continuation vehicles. These vehicles give GPs more flexibility to hold onto valuable assets, but they raise concerns about pricing, rollover decisions and potential conflicts of interest. For LPs, fairness and transparency are paramount when evaluating these options.

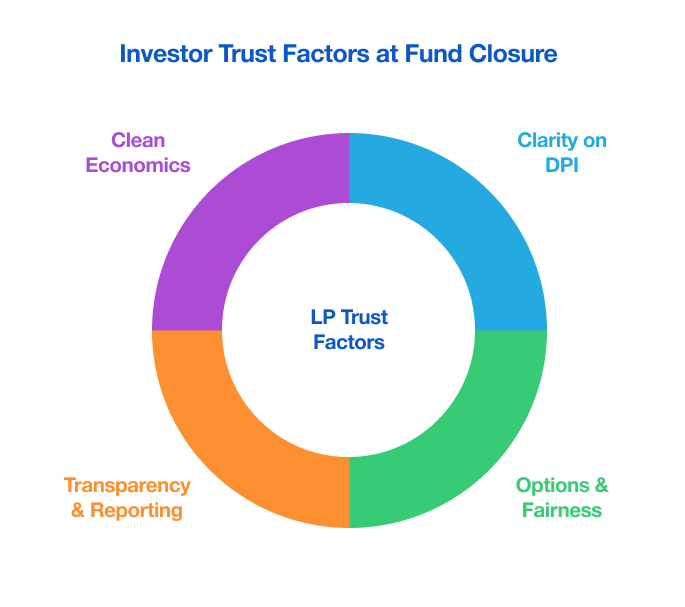

What LPs really want

Whether they are global institutions or Indian family offices, LPs share similar expectations when it comes to fund closure:

- Clarity on DPI: LPs want to know how much of the Total Value to Paid-In (TVPI) has been converted into DPI.

- Fairness in Continuation Fund Structures: LPs seek real choices and transparent pricing when it comes to continuation funds.

- Regular Updates: Investors expect quarterly reports on key metrics such as DPI, TVPI, IRR and PME benchmarking.

- Transparency: LPs have little tolerance for hidden fees or opportunistic resets.

Best practices for fund closure

Smart fund managers begin planning for closure 18 to 24 months before the fund’s expiration. During this period, each portfolio company should be mapped to its most likely exit strategy whether through a trade sale, IPO, secondary market transaction, or continuation vehicle. Early communication with the LPs is vital, especially if continuation vehicles or dissolution periods are being considered. Transparency is key to ensuring that investors are never taken by surprise.

During a dissolution period, ideally no management fee is to be charged to align interests with the LPs. Secondary processes should be competitive and well-documented to eliminate any doubts about fairness. When the final distribution is made, LPs should receive a comprehensive closure report that outlines every asset, exit and the results in comparison to agreed-upon performance metrics.

“Closure done well is not compliance; it’s trust-building.”The bigger picture

Fund closure is as defining as fund launch. LPs remember how you end. A clean and transparent closure can serve as a powerful credential when raising future funds.

In India, exits remain uneven, SEBI regulations are tightening and investors are demanding real liquidity. For emerging managers, closure may be the ultimate test of credibility.